Should I Buy a House as a Single Person?

Posted on Jun 01, 2022

Is it hard for a single person to buy a house? This question is often at the forefront of people’s...

Posted on Jun 01, 2022

The U.S. housing market has been appreciating rapidly, with the median listing price climbing from $376,500 this January to $424,100 in April. For homebuyers who were already struggling with the high prices, it was incredibly demoralizing to see prices jump that dramatically - without seeing any increase in quality or size, or any decrease in competition.

Buyers still have to jump through hoops, waive contingencies, and pay over asking, which has a lot of people wondering if it’s a good time to buy a home in the first place.

Will you lose money buying a house right now? No - not if you do it right. Here’s why.

In today’s investment-savvy world, many would-be homebuyers are worried about having the rug pulled out from beneath them. But a house is never a bad investment because there is a big difference between putting your money in property and, for example, putting your money into a cryptocurrency.

If a cryptocurrency stops appreciating and the coin loses value, investors are often left with absolutely nothing. If a house stops appreciating value, though, you still have a house. If a house loses some value (which is unlikely), you’re still not paying rent - and the house will eventually be paid off. In other words, you're still accruing equity no matter what.

According to the Survey of Consumer Finances, the difference in net worth between renters and homeowners is staggering. Homeowners have a median net worth of $255,000, while renters have a net worth of just $6,300. Buying a house is ultimately one of the most dependable ways you can build your personal net worth in the U.S. - so, no, it’s not dumb to buy a house right now. It’s an investment in your future.

Last year when people were claiming the housing market was due to crash, we covered just how frequently both experts and laypeople believe a crash is imminent - and they’ve continually been wrong.

Data just doesn’t back this as a likely outcome - so if you’re trying to time the market, you’ll probably just time yourself into paying even more for a house by waiting.

The last housing crash was traumatic even for those not directly impacted by it, and many people absorbed the idea of high home prices = housing crash. Despite what our memory may lead us to believe, though, housing crashes are historically a rare event - and even when they happen, the value of homes always bounces back eventually.

How is today different from 2008?

Keep in mind that there is incredible demand for homes right now from millions of millennials who are coming of age and want to buy homes. As long as there’s huge demand, prices won’t come down, which means that a catastrophic economic event would need to happen that effectively makes it impossible for those millions of people (likely including you) to not own a home.

In other words, if you think you’d profit from a housing crash: in all likelihood, you wouldn’t. Instead of trying to time the market, meet with a mortgage advisor and find out what your options are today for financing a home (and you have more than one option), rather than in a theoretical tomorrow.

Still convinced the market is about to peak and crash? Just review these tweets that capture people feeling the same way, every single year.

To benchmark these tweets: the median home price in Aug. 2018 was $283,000. For anyone who was waiting for a crash, hindsight tells us it never happened. Instead, had they bought that home it would be worth about $424,100 today. In total, almost $150,000 in appreciation.

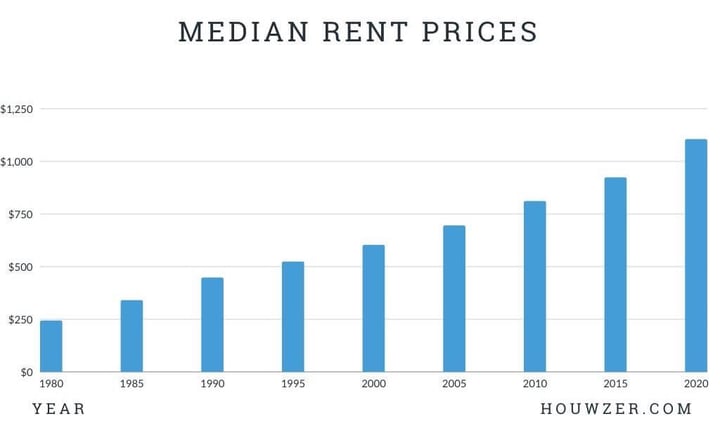

And if they spent that entire time patiently waiting for the market to crash? They’ll likely have spent about $54,000 in rent (calculated from the U.S. average rent price over this time period). That’s some serious equity they could’ve been putting into their own home instead of their landlord’s.

Just remember that if today’s prices look high, tomorrow’s prices probably won’t look a lot better.

When you buy a home, you should always have at least a 5-year plan in place. This is because there are sizable costs associated with both buying and selling a home - so even with appreciation, it will take you several years to generate a net profit.

You might be worried about what happens to your mortgage during a housing crash, but in reality little will change. You can temporarily become “underwater” on your mortgage - this means that due to falling home prices, you now owe more on your mortgage than the home is worth. So yes - in this sense, it is possible to “lose money” if you buy a house right now, because if you had to sell it immediately you would have to pay the bank to cover the difference between the lower current value and what you owe.

However, lenders don’t care if you’re underwater on your loan - all they care about is making sure you can pay your mortgage bills every month, and the amount you pay each month is already pre-determined. So if you have a long-term plan for living in your home, you may never even realize that you were underwater on your mortgage, if the market rebounds by the time you’re ready to sell.

Although the '08 crash wasn't great for home prices, the median U.S. home price had rebounded to the pre-crash peak six years later.

And even if life circumstances require you to move out of your house immediately after a recession - when your home’s value has dropped like a stone - keep in mind that the rental market never experienced the same dramatic dip the housing market did. So renting out your home while you wait for the market to rebound is always a viable option.

It’s always possible that we’re on the verge of an economic recession. With political upheaval, wars, a pandemic, and inflation all happening at once, the economic future becomes more opaque and unpredictable.

But if you're wondering whether you'll lose money buying a house right now, rest easy: the market always rebounds, and if you have to move before that you have options (like renting) to help maintain your equity.

However, there are certain measures you can take to protect yourself from being the guy left holding the empty bag.

Be wary of paying an incredible amount of money over asking. In this red-hot market, sometimes buyers have to go 15, 20, or even 50% over asking in order to get their offer accepted.

Sometimes paying over the appraised value is just the reality of appraisals: because they rely on comps (which are historical), they often lag behind when the market is rising very quickly. However, a word of caution is needed here, because it can mean you end up paying way more than what the next person would pay if the market cools off. Follow your agent's advice and don't react emotionally - only buy a home if the numbers check out.

Again, having a 5-year plan for your house is key. If your comfort with your investment is reliant on the market rising 10-20% each year, you’re putting yourself in a risky position. Homeowning is a long-term investment strategy - it shouldn’t be used for short-term gains unless you’re willing to accept the risk.

Subscribe to our newsletter to get essential real estate insights.

Posted on Jun 01, 2022

Is it hard for a single person to buy a house? This question is often at the forefront of people’s...

Posted on Jun 01, 2022

Be prepared with these 5 tips on home buying So you’re ready to buy your first house, eh?...

Posted on Jun 01, 2022

The housing market may have been nuts, but the rental market last year wasn't much better. Millions...