The Second-time Home Buyer Experience

Posted on Jun 16, 2021

According to Rocket Mortgage, first-time home buyers live in their homes for an average of 11 years...

Posted on Jun 16, 2021

We’ve written about just how crazy this market is before, with homes in hot areas going for as much as 50% over asking price. Many people who want to move are wondering: should I sell my house now and rent until the market cools down, then buy my next home?

There are both benefits and drawbacks to renting while you wait out the market: the right answer will depend on your unique situation and ideal timeline. First, we’ll cover the potential drawbacks of renting - then, we’ll discuss when it might be in your best interest to rent.

When's the best time to buy a house? You might assume that the housing market has to cool off eventually - and it might. However, there are many stories of people who were ready to buy a house 2-3 years ago but they, too, were waiting for the market to “cool down.” The homes they thought were “too expensive” in 2018 are now selling for $100,000 more - and those renters are kicking themselves now.

Even experts in the housing market can call it wrong: CNBC interviewed several experts in 2018 who were calling it "a better time to rent than to buy” and noted that “sellers are starting to see demand fall off a bit, as buyers hit an affordability wall.” Rather than seeing a real drop in demand, though, prices rose steadily upward. The median home listing price was $290k in May 2018; three years later, it's $380k (via Realtor).

In other words, one big drawback of renting while waiting for the housing market to cool down is risk: you might end up spending thousands of dollars on rent - paying off someone else’s mortgage - only to find that homes in a couple of years are even more expensive than they are now. Of course, the market may cool - it’s really a question of how comfortable you are with the risk.

“The downside to renting is that you’re paying someone else’s bills - you don't have equity. In some cases the rent cost is higher than their actual mortgage costs would be,” notes Virginia-based Realtor Pamela Debnam.

Issues with timing the market: The Case-Shiller U.S. National Home Price Index shows that since 1987, the only time prices really fell was in response to the 2007 sub-prime mortgage crisis. Source: FRED

One thing that could cool the market a bit is mortgage rates, because low rates have helped drive high demand: but that won’t necessarily be a good thing if you’re looking to finance your new home. If you opt to rent for a year or two, you could miss out on the current historically low home loan rates. Even a half-point difference in your rate can mean paying many thousands of dollars less over the lifetime of your loan.

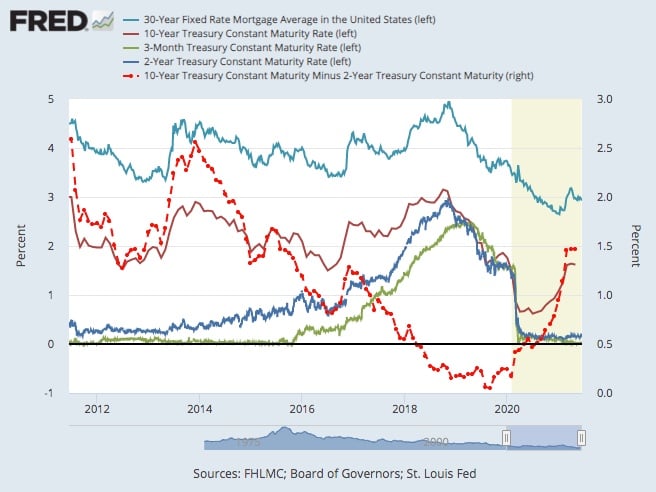

Generally speaking, mortgage rates follow the yields on the 10-year Treasury note - and yields hit an all-time low when COVID-19’s impact hit the economy. As the economy ramps up, yields - and therefore mortgage rates - are expected to rise.

By opting to rent for a year or two rather than buying, it’s possible you might see demand for homes (and therefore home prices) fall - but if mortgage rates rise, you might pay thousands more in interest anyway.

The 30-year mortgage rate roughly follows the 10-year treasury rate. Source: FRED

As a seller, your biggest worry might be that once you sell your home, the ultra-competitive market will prevent you from buying your next home right away - and no one wants to end up homeless. However, it's important to remember that sellers have the upper hand in negotiations right now. One tactic that has been gaining popularity is the seller rent back.

A seller rent back (also known as a post-occupancy lease) allows sellers to continue living in their home even after closing - giving them time to find a home that works for their budget. They essentially "rent back" their home from the next buyers for an agreed-upon length of time, which can be weeks or months. For sellers who have been hearing about how ultra-competitive the market is, this can be a great option.

“I’ve been fortunate enough to get prospective buyers, when they submit their offer, my [listing] clients get at least a two-month rent-back as part of the offer to find their next property. That gives them time to not feel pressured to move right away,” explains Maryland-based listing agent Brian Cooper.

Rental restrictions are an expected part of rental living, but they can be a rude awakening for homeowners who have gotten used to having whatever pets they want, hanging anything up on the walls, and arranging their space as they see fit. And while you’re no longer in charge of fixing a broken water heater or a leaky pipe, you may have to deal with unresponsive landlords instead (according to Avvo, 33% of renters say their property manager is slow at making necessary repairs).

“There are so many restrictions with what you can do, and that can be quite an adjustment for someone who has purchased their own home to move into a rental property,” observes Debnam.

Renting also means less control over your housing situation: if you sign a year-long lease, there’s typically little flexibility for leaving early. Conversely, if you sign a month-to-month lease, you might have only 60 days to vacate the apartment if your landlord decides to sell it or rent it out to a family member.

Renting can be in your best interest if your plans for the future are unknown - or if you know you’re going to move soon.

In a hyper-competitive market, people often need to pay more than the appraised cost to win their home, and can potentially end up owing more than the home is worth if the market cools. Most of the time, because home prices appreciate, homeowners are fine so long as they stay in their homes for several years. They continue to pay down their mortgage, the home gains value, and they’re able to sell at a profit. If circumstances require you to move within a single year or two, though, there’s more risk involved.

“If they plan to stay two years, I would say don’t buy. Because we are at an all-time high and it will definitely start to go down at some point,” advises Debnam. “I really feel that they need to have at least a 5-year plan if they’re planning on purchasing in this market.”

Cooper says clients should focus on their long-term goals with their property. “Many of my clients understand the market, and they understand what the market should look like in normal situations. I say to them: What are your long-term goals? If you’re only here for three years because of your job, it might not be cost-effective to purchase right now.”

The other thing to consider is closing costs. When you buy a home, there are mortgage origination costs, title insurance, the appraisal, the inspection, a deed recording fee, and more: altogether, these costs can be 5-7% of the purchase price - a significant amount of money. When you sell your home, there are Realtor commissions to pay as well. And whether you sell or buy, you’ll likely pay transfer taxes (in PA, for example, the transfer tax is 2.14% of the purchase price, split between the seller and the buyer - in other words, thousands of dollars).

Closing costs are an anticipated part of home sales, but if you plan on moving within a couple of years of buying your home, then renting may help you to hold on to more of your equity. This is actually known as the "Five-year rule" in real estate: new homeowners should plan to stay put for at least five years before selling their property so that the value the home gains through appreciation exceeds what they lost through closing fees.

Cash buyers have an advantage when it comes to timing the market because they don’t need to worry about rising mortgage rates. If you’re going to pay for your home in cash, you can rent for several years without having to worry that an increase in mortgage rates will force you into a smaller home later on.

If you can choose to use cash, "It makes more sense to become a cash buyer when rates are high so you can leverage your money better," explains mortgage advisor Robert Wagner. "As rates go up, an individual’s buying power decreases."

There’s no right or wrong answer when it comes to what you should do after you sell your home: rent and wait, or buy the next one? Your brokerage, after all, will still be able to help you no matter when you decide to jump in the game.

Cooper emphasizes that regardless of whether homeowners opt to buy or rent, the time to sell is now. “A lot of clients are iffy as to whether they should sell and then move,” he says. “I’m advising them: if you’re serious about selling, now’s the time to sell because we don’t know what the market’s going to do in the next month, or the next three months, or the next six months.”

Ultimately, Debnam advises that sellers who are also looking to buy shouldn’t get discouraged by the competitive market. “What they are going through is what others are going through as well. Don’t let offer rejections get you down; keep pushing forward,” she says. “I submit as many offers as it takes on behalf of my clients, so as long as they stay in it, I am in it with them, and we just keep moving along until we find them a home.”

Subscribe to our newsletter to get essential real estate insights.

Posted on Jun 16, 2021

According to Rocket Mortgage, first-time home buyers live in their homes for an average of 11 years...

Posted on Jun 16, 2021

Mortgage rates have been on a journey this year - and it’s the sort of journey that makes buyers...

Posted on Jun 16, 2021

Is it the right time to buy a home? For many people, the answer is “yes.” Surprising though this...