The Great Housing Reset: What to Expect in 2026

Posted on Apr 13, 2022

Forget the frenzy of 2021 and the freeze of 2024. We're entering something entirely different: the...

Posted on Apr 13, 2022

One of the (many) reasons the housing market has been so hot lately is the historically low interest rates for homes. The lower your mortgage rate, the more house you get for your money, essentially. As a result, many buyers have continued to try and land a home - despite the crazy competition.

In 2022, however, we’ve seen interest rates slowly start to rise. They're currently hovering around the high 4s, and industry experts predict that the year could end with average rates as high as 5.5%. While this is still low historically, it’s not the crazy low of January 2021, when they dipped below 2.7%.

A rate increase of just 1% can add up to hundreds of dollars a year, and many thousands over the lifetime of your loan.

“Rates are definitely going to pick up slightly,” notes Orlando-based buyer agent Jeffrey Colom Ortiz. “It’s already happening - we started out the year at 3.1%, compared to last year when we were in the high 2’s. This directly impacts what you can qualify for.”

If interest rates do rise as they’ve been predicted to, what’s going to happen? Here’s what you need to know.

Sometimes it can be difficult to understand the impact of rising interest rates when you don’t have specific numbers.

Let’s say you’re buying a $450,000 home with 10% down ($45,000) and opting for a standard 30-year loan.

Using Bankrate’s Mortgage Calculator, you can see that:

In other words, over the lifetime of the loan, the difference of just 1.5% means you pay over $100,000 more. That’s a lot of money - and it’s easy to see why home buyers are willing to compete so hard right now.

Rocket Mortgage Insights spells it out further: “Every quarter-percent (.25%) rise of interest rates reduces homebuyer purchasing power by about 3%. That means for a home purchase of $300,000, a 1% interest rate rise reduces buying power to just under $267,000.”

Going $5,000 over-asking is not so crazy sounding once you realize that it allows you to put equity into your own home sooner, and ensures you get a lower mortgage rate before any major hikes happen. So if you're ready to lock in your mortgage rate, don't wait.

“Rising rates will be a wake-up call for both sides. Eventually, if the prices keep going up, it’s just going to kick a lot of people out of the market. A lot of the people who could previously buy, are going to be unable to buy - unless the prices come back down,” explains North Virginia-based Realtor Joy Khalil.

There’s an advantage to interest rates rising, though, and that’s decreased competition. When rates rise, some buyers are pushed out of the market because they can no longer comfortably afford the home they want and they need time to save. Decreased competition means that you're a lot less likely to get rejected 10 times in a row - and you'll have more leverage to keep the price reasonable.

Home buying also becomes less lucrative for investors because higher interest rates make borrowing money a more expensive endeavor. In 2021, nearly 15% of homes for sale in the U.S. were purchased by investors. That’s the highest percentage in two decades, and it happened while many first-time homebuyers were fighting tooth and nail to get a house. It’s hard to compete with investment firms that can buy homes in cash and can afford to go over-asking every time.

Keep in mind: the more you can save to put down on your home, the less you’ll be impacted by interest rates rising. However, make sure you understand the benefits and drawbacks of waiting until you have 20% down.

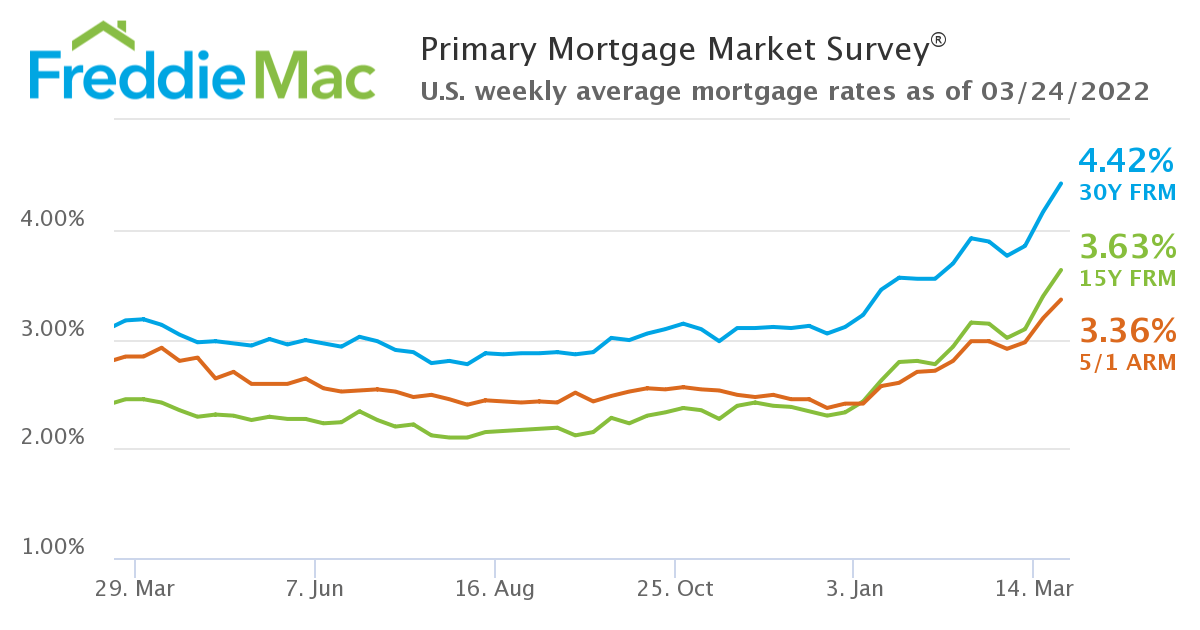

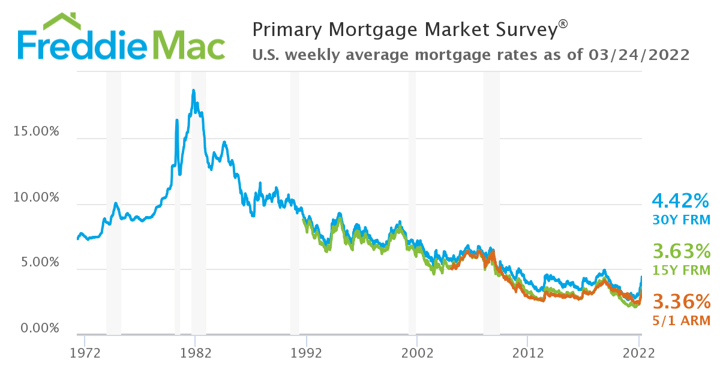

Also, keep your chin up! While interest rates are rising, data from Freddie Mac shows that mortgage rates are still relatively low. The rates we’re seeing now are still a steal compared to what most people had to pay at any point over the last three decades.

Historically speaking, interest rates are still great - and buyers shouldn't be panicking over a slight increase.

For home buyers, rising interest rates are:

If you’re a home seller, rising interest rates may actually have a net neutral effect on your home sale experience - because home sellers are typically home buyers, too.

"Typically in a market where interest rates are higher, we see a slowing of the sales for the sellers. So sale timelines usually take longer."

On the negative side, you may receive fewer offers for your home, and the offers you do receive might come in close to the asking price or under asking - rather than the crazy 20%-over offers some high-demand homes saw last year. Homebuyers will have more constrained budgets to work with as their estimated monthly mortgage payments rise with each uptick of the mortgage rate.

“Typically in a market where interest rates are higher, we see a slowing of the sales for the sellers. So sale timelines usually take longer. Nowadays sellers are getting offers in less than a day to three days if their house is priced right and if it’s halfway decent,” explains Khalil. “As interest rates rise, buyers have to lower what they can afford. So the circle of buyers who can buy your home now is shrinking as the interest rates go up. Sellers haven’t quite gotten the message yet, but they’re going to. Their house is going to start sitting. We might not see prices drop below what they were, but we might see a slowing in the increased value.”

On the other hand, most home sellers are home buyers, too, so if offers come in lower for your home, this might mean you get to pay less for your next home. The decreased competition could make it easier to time your home sale/home purchase as well. When the market was super hot, many sellers essentially became trapped in their homes because they couldn’t afford to sell their homes, knowing it might take many months to buy the next one.

The other thing you should keep in mind is that a home purchase is an important milestone in many peoples’ lives, and often represents a need rather than a want - whether that’s to build equity, prepare for a growing family, or move from the city to the suburbs. Because this is such a big life decision, most buyers are going to stick it out and continue looking for a home. The market is unlikely to shift dramatically for many years, since we’re going to have the problem of too much demand and not enough homes to go around for a while.

For home sellers, rising interest rates are:

"A lot of people I’ve been meeting have been building homes because they can’t find existing homes to purchase. Despite their homes not being ready until next December, they want to sell now, because they know for sure they can get a high price - and they don’t know that will hold true tomorrow,” notes Khalil. “The market might keep going up - it’s been such a whacky market it's not following rules. And to be honest, that has always been the case. No one has a crystal ball. But we have so many things going on in the world right now between the pandemic, the war, the markets, the gas prices - there are so many unknowns and we’re not in the stable, predictable place that we used to be. I can say: today, you’ve got a good price. Take it today, because tomorrow might be totally different.”

Subscribe to our newsletter to get essential real estate insights.

Posted on Apr 13, 2022

Forget the frenzy of 2021 and the freeze of 2024. We're entering something entirely different: the...

Posted on Apr 13, 2022

As interest rates drop to historic lows and the economy remains uncertain, many homeowners are...

Posted on Apr 13, 2022

Economic headlines can feel unsettling: rising inflation, fluctuating mortgage rates, and talk of a...