Should I Buy a House as a Single Person?

Posted on Mar 03, 2023

Is it hard for a single person to buy a house? This question is often at the forefront of people’s...

Posted on Mar 03, 2023

Mortgage rates have been on a journey this year - and it’s the sort of journey that makes buyers very wary of entering the market. Many are waiting, hoping that rates will fall a point or two - allowing them to save $100 or more on their monthly mortgage payment as a result. But is this a good plan of action? Here’s what you should keep in mind.

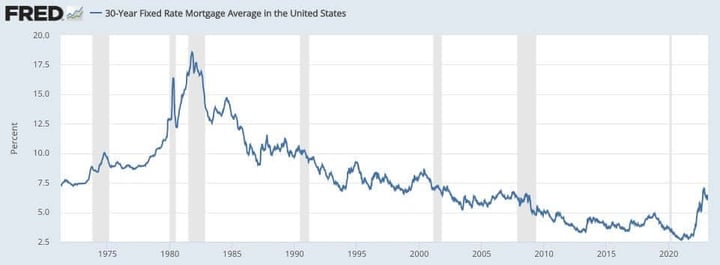

The question “do high rates mean it’s a bad time to buy” is misleading because it assumes something that isn’t quite true: that the rates today are “high.”

Are they high compared to last year’s rates: definitely! But if you want to wait around for 3% to hit again, you might be waiting for several decades. Or forever.

It can be tough to give up on the dream of a 3% rate, especially when so many people you know may have received such a rate just a year ago.

However, by historical standards an incredibly low rate was an anomaly - and ultimately it led to skyrocketing home prices. Once buyers were able to buy more… they did! And now the buyers with low rates are reluctant to sell their homes and give up their low monthly payments, further limiting housing inventory and making it difficult for prices to come down.

Homebuyers dislike rising mortgage rates because it means an increase in monthly payments. A single percentage point can mean an extra $100 a month, purely in interest. However, there's a good chance you don't need to deal with the high rate for the lifetime of your loan. Here's why.

You might not love the rate you receive, but you aren’t necessarily stuck with that rate forever.

In other words: date the rate, but marry the house. How does this work?

If the interest rate drops in the future, you’ll have the option to refinance. This means you replace your current loan with a new one. When that happens, not only will you receive a different interest rate - you can also opt for a different loan term. If you’ve already paid off a few years of your mortgage, refinancing to a 15-year mortgage could shave thousands of dollars of interest off the lifetime of your loan - and your monthly payment might not change by much.

On average, refinancing costs around $4,000. If you think there's a chance the rate could drop far enough to make a difference, you can try asking for $4,000 in seller assist at the closing table - meaning that the seller credits you that money at closing - then use that to refi a new loan if the rate drops. And if the rate doesn't drop? You're no worse off for having gotten in early and started the journey of building equity!

Since there’s no guarantee that rates will ever drop, your financial plan should not be reliant on that happening. Luckily, your lender isn’t going to approve you for a loan you can’t afford (this protects them - but it also protects you). So even if the current rate is hard to swallow, you should be able to budget and make it work.

"It's important to stick to your budget - you should never be house poor," advises Jack Mager, a Baltimore-based Houwzer Realtor. "Your payment should not be a burden. So start with a cheaper house, buy a town home. Have a payment you can afford. A year, two years down the road refi at a lower rate."

Keep in mind that there are other ways of lowering your rate, too. If you know for sure that you won’t stay in your home for the full 30-year term, you might want to consider an ARM (adjustable rate mortgage). ARMs today come with a fixed interest rate for the first several years. A 7/1 ARM, for example, will give you seven years of a fixed rate - and it’ll be lower than than the average 30 year fixed rate, usually by at least .5 or more. If you sell before year 7 hits, you never have to worry about the rate adjustment.

Want to know more about your mortgage options?

Talk to a Houwzer mortgage advisor

(it's free and there's no obligation)

Once you buy a home, you can start breathing easier because your payments are locked in place. Although taxes and insurance costs may go up over time, the bulk of your mortgage payment isn’t going to change.

Within just a few years, you’ll start to see the impact of having a fixed payment. Rather than having to deal with constantly rising rental prices, you get to avoid the battle with your landlord over price entirely. And rent always goes up. Even during the '08 housing crash, rental prices still went up.

"Even though it's a little more expensive at the moment, buying is still way better than renting," says Jack. "Because every payment you make to a landlord feeds the landlord and his mortgage. It's never coming back to you."

Keep in mind that the cost of housing is relative, and people rarely think homes are a reasonable price. Here are three examples of people on Twitter who found housing prices unreasonable in 2015:

In San Diego prices may have seemed high in 2015, but compared to now, they’re a steal.

Let’s say they had decided to just stomached the "high price" instead of hoping for prices to fall (which, as we know, they didn’t).

Had they purchased an average-priced home (average at the time was $200,635) with 5% down, as of today they’d have paid $39,000 toward their mortgage, they’d be sitting on around $200,000 in appreciated equity (the average-priced home is now hovering around $400,000), and their current payment of around $1,100 would be far lower than what the average homebuyer (or renter) is dealing with today.

As crazy as it may seem, the home prices we see this year are likely to to be some of the lowest we see going forward. Even if home values take a slight dip, you’re not going to notice it much so long as you hold onto your home for several years.

Keep in mind: buying a home and planning to sell it within the span of a couple years is never a great idea, because it won’t allow you enough time to accrue equity and cover closing costs. For situations where you know you’ll only be there a year or two, you may be better off renting.

You might be thinking that this is the worst time in all history to buy a house. But in some ways (not all ways, but some) you can benefit from the current environment. Why?

There is far less competition for homes right now than there was a year or two ago. Not only are there fewer individual buyers - investors are fleeing the home-buying market. Bidding wars? In many situations, you’ll be the only offer. This allows you a bit of negotiating power.

Many buyers today are asking the seller to buy down the rate for them. 2-1 buydowns - where you receive a rate 2% lower the first year, and 1% the second - are a popular option. This allows you some breathing room to adjust and build up your savings after buying your home (and also allows time for the rates to come down, if you’re interested in refinancing).

You can also get more aggressive with your offer price. Should you offer 20% below asking? Probably not. But don’t be afraid to push the envelope a little, especially if the home has been on the market for months and the seller likely understands that they might not get as much as they were originally hoping for.

"What we see in the market right now is: Inventory is still very low. Way lower than it should be. Prices are still high - but not as crazy as they were a year ago," explains Jack. "Due to the rates, there's fewer buyers. While there are still multiple offer situations, clients are actually able to negotiate more contingencies, etc. than they were a year or 18 months ago."

On average, a home's value increases by 4% each year. So if you're wondering, should I wait to buy a house? Consider how much you could benefit from the increase in equity that would likely occur while you're waiting.

"During that time, home values appreciate. They may take two or…three years, maybe five years. But you're gonna make up for that money, your house is going to be worth way more than when you bought it," explains Jack. "So that is why I say, don't worry about that mortgage rate too much. If the mortgage payment is $250 more than it could have been two years ago, so long as you can pay for it, don't worry about it - you're going to make up for it."

There is no magic 8-ball for mortgage rates (we'd be the first to give it a shake).

Right now the mortgage rate is high in large part due to the U.S. government looking to curb inflation. Because this has been a persistent issue this year, we're unlikely to see rates drop too much for this reason alone.

Here's what industry experts are predicting:

Something to note: the U.S. 30 Year Mortgage Rate averaged 7.75% from 1971 until 2023, so we're still below the historical average.

If you don't want - or can't - deal with the current interest rate, one thing you can do is find a Realtor and get your ducks in a row. That way if the interest rate does drop - like it did for a few months this winter - you're already ready to go and first in line.

(it's free and there's no obligation)

Subscribe to our newsletter to get essential real estate insights.

Posted on Mar 03, 2023

Is it hard for a single person to buy a house? This question is often at the forefront of people’s...

Posted on Mar 03, 2023

Be prepared with these 5 tips on home buying So you’re ready to buy your first house, eh?...

Posted on Mar 03, 2023