Washington DC Regional Q4 Housing Report: Strongest Market in 15 Year

Posted on Oct 01, 2021

Posted on Oct 01, 2021

When Biden became president last year, one of his priorities was to address the issue of housing affordability. Since election day, Biden and his team have proposed a wide range of potential solutions to the current issues.

So how could these changes end up impacting the overall housing market - and are there potential unforeseen consequences? Here’s what you need to know.

One of Biden’s plans (as part of the larger American Jobs Plan) for the next eight years is to subsidize the development, maintenance, and retrofitting of affordable housing units. Both the cities and suburbs would benefit.

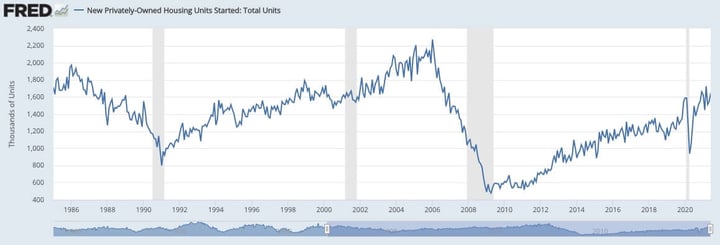

The subsidies are considered necessary because it’s not currently as profitable for developers to create affordable, lower-cost housing (the current price of lumber has been a hot topic lately), which has been pushing up the cost of housing for everyone. Entry-level construction sharply declined after the 2007 housing crash, and builders are still playing catch-up.

If this plan goes into effect, it could have a real impact on the housing market. Right now, competition is driving prices up higher than ever before: there are too many people and not enough homes. By offering more of the most affordable homes, it will be easier for everyone to find a home that’s actually in their price range.

Biden’s plan also encourages communities to build affordable housing in middle and upper-class communities, which can help address a variety of disparities. For example, people will be able to obtain affordable housing near where they work or go to school.

The proposed first-time homebuyer tax credit aims to put money back in the pockets of Americans who are investing in the housing market for the first time. If the bill is successful, first-time homebuyers would be eligible for a one-time tax credit of 10% of the home’s purchase price, up to $15,000. Most homeowners would end up qualifying for the full $15,000 by spending at least $150,000 on their home, since the average American home purchase price is now $285,000. To qualify, homeowners can’t make over 160% of the area’s median income.

Because this is a tax credit, if a homeowner owes $10,000 in income taxes and claims the $15,000 credit, then they would receive a $5,000 refund on their end-of-year tax filing. In order to keep the credit, homeowners would need to keep the home as their primary residence for at least four years - otherwise, they have to repay a portion of the funds.

Will this impact the housing market? It’s hard to say how it would impact the market at large, considering just how competitive the current market is for buyers. Because homebuyers receive the credit long after buying the house, it shouldn’t drive home prices up.

But what it will do is offset the financial hit of buying a home, particularly for buyers who are nervous about tying up all of their cash in a home purchase. Closing costs can be a significant hurdle for first-time homebuyers, and while they would still need cash upfront, a $15,000 tax credit could help replace lost savings.

Biden’s proposed Downpayment Act would give $25,000 to first-generation homebuyers to use toward their closing costs. The requirements for these recipients would be tighter than for the first-time home buyer credit: homebuyers can’t make more than 120% over the local median income, and they need to be first-generation home buyers. In Philadelphia, for example, the median income for an individual is $26,211 as of 2019 - so an individual could make no more than $31,453 and still qualify.

This bill is really aimed at helping marginalized communities who might otherwise be priced out of the housing market, which can have a positive and uplifting impact and helps to break down the long-lasting impact of past discriminatory housing policies and longstanding racial inequity.

“Down payment and closing costs are often the single greatest barrier to homeownership,” notes the Department of Housing and Development (HUD). “Minority families lack the accumulated wealth for down payment and closing costs.”

Helping first-generation homebuyers with their closing costs could help to break the cycle of poverty many families face. Owning a home has, historically, been one of the most predictable ways for Americans to build wealth (this is why Houwzer launched the RiseUp Fund, which is providing down payment and closing cost assistance to the underserved).

On the other hand, it could have the unanticipated impact of heating up the housing market even more. If more people are able to buy a home, it will increase competition for the extremely limited available affordable housing stock. And when demand goes up, prices tend to rise as well – which could disproportionately impact people who are already struggling to afford a home.

Over the past several decades, zoning laws have become a way for communities to enforce a sort of economic segregation by way of keeping affordable housing out of middle and upper-class neighborhoods. Laws stating that only single-family homes can be built in certain areas, for example, keep many lower-income earners priced out of the area completely.

This has led to greater issues of accessibility - many low-wage earners can no longer afford to live in the very areas they work in, and often need to travel great distances to get to work. Zoning laws contribute to the affordable housing crisis by making it difficult to build multi-family units, and lead to segregated neighborhoods.

Overturning zoning laws would likely result in more affordable housing - which in turn, would make the housing market more affordable for everyone.

The situation is nuanced, though. Although NIMBYs, or people who say “not in my backyard,” have typically been seen as affluent neighbors wary of an influx of low-income housing, the Philadelphia Inquirer points out that in Philadelphia, at least, many of the concerned families are actually low-income earners themselves who are wary of their historic neighborhoods being trampled.

They point out that: “Gentrification in Point Breeze [neighborhood] merits some regulation due to the destruction of a low-income community with a high rate of Black homeownership. New multifamily developments with only one-bedroom units and no parking will not bring more low-income families to Point Breeze.”

On top of that, it’s currently envisioned as a voluntary grant program – meaning that already-prosperous cities could opt out of participating and keep their restrictive zoning laws. Because the proposed system only rewards, rather than penalizes, many have been calling it Biden’s “all carrot, no stick” approach.

The price of lumber and steel in the U.S. has risen this year for several reasons. The Trump Administration wanted to encourage job growth and industry growth in America by imposing tariffs on imported goods in 2017/18 (such as a 9% tariff on Canadian lumber).

While this move has helped those industries thrive, especially during COVID, it caused the price of lumber and steel (and therefore new homes) to quickly rise. According to an analysis by the National Association of Home Builders, new homes were $36,000 more expensive on average due to the price of lumber alone, as of April. Although the price of lumber is starting to come back down, this highlights just how dramatically a shift in the price of goods can impact construction.

On top of this, COVID-19 inspired a lot of people to either move homes or own for the first time, which created a further squeeze on the market.

Plenty of industry groups have been asking the White House to lift the tariffs. This would likely help to cool down the housing market over the next few years by lowering the cost of both new homes and renovations on existing homes. However, it remains to be seen whether this will happen, since dropping the tariffs could negatively impact American lumber and steel jobs – so not everyone is advocating for this.

If Biden’s policies are put into place, they could positively impact the housing market in numerous ways - more affordable housing could become available, and first-time homeowners may get a helpful boost when they go to buy.

However, it remains to be seen whether these plans will be implemented - and if they’ll be implemented the way they were envisioned. If a plan pumps more money and/or more homebuyers into the housing market without simultaneously increasing the housing stock, it could have the unintended effect of pushing competition - and therefore home prices - even higher.

Subscribe to our newsletter to get essential real estate insights.

Posted on Oct 01, 2021

Posted on Oct 01, 2021

Houwzer’s Senior Economic Advisor, Dr. Kevin Gillen, has released his Q3 housing market report for...

Posted on Oct 01, 2021

Houwzer’s Senior Economic Advisor, Kevin Gillen, has released the Q1 housing market report for the...